Originally published in June 2016. Last updated on July 23, 2025.

Starting or growing a successful service business requires more than passion and dedication—you need funding to make it happen.

As a business owner, you might not have the personal savings to cover your initial or changing business needs, but you can always apply for a loan. If traditional loans seem out of reach, don’t worry, there are several other options for financing.

Understanding how to get a small business loan can help you secure the funds you need without draining your personal savings. Keep reading to learn the best way to obtain small business loans in 8 steps to finance your business’s future.

8 steps to getting a small business loan:

-

Decide what you need the small business loan for

-

Know your loan options

-

Review different small business lenders

-

Determine your eligibility

-

Create (or update) your business plan

-

Gather your service business’s financial information

-

Apply for a small business loan

-

Get approved and review your loan agreement

1. Decide what you need the small business loan for

Lenders want to know how their money is going to be used and whether they’re likely to see a return on investment. Before you approach a lender for a loan, you should know:

- What you need the loan for (be specific)

- How much money you need

- How long it will take you to make it back

Some reasons you might want to take out a small business loan include:

- Marketing a new business

- Equipment purchases or upgrades

- Expansion of services or location

- Hiring new technicians

Once you have those answers, gather as many details as possible and back up your request with numbers.

For example, if you want to start a lawn care business and need to purchase a vehicle, make sure that you know how much it will cost, how it will contribute to your business growth, and when you expect it to become profitable.

Get quotes for each potential cost and create a small business budget. Use financial statements demonstrating growth from similar efforts and calculate your predictions for growth, including best- and worst-case scenarios.

If you’re going to open a new location, for example, you’re not doing that overnight. You need to build that into the budget and know the exact details for forecasting.

If you aren’t sure what you need or where to find these numbers, work with your accountant or visit your local small business association for guidance. You can also use a good accounting app to get started.

Having a clear and realistic goal backed by a strategic plan for growth will increase your chances of getting approved.

2. Know your loan options

There are several types of small business loans, and it’s important to pick the right ones to apply for. This will depend on several factors, such as:

- Whether you need one-time or ongoing funding

- How quickly you need the funds

- Your business’s credit profile

Here are some common types of small business loans:

- Term loans: A lump sum of cash that can be used for business expenses, including marketing, payroll, renovations, and expansions. You typically repay term loans in monthly installments.

- Lines of credit: Flexible loan that lets you tap into capital as you need it to cover expenses such as payroll or unexpected repairs

- Equipment financing: An asset-based loan used for purchasing new or updating equipment. The equipment is typically used as collateral, and lenders can seize the equipment if the loan is not paid.

- Business credit cards or personal loans: Credit cards or personal loans may be a good option if you’re just starting out your business and might not qualify for other types of loans.

There is also a Small Business Administration (SBA) loan. The SBA exists to help small business owners and entrepreneurs succeed. An SBA loan is a loan that is partially guaranteed by the SBA.

The SBA doesn’t lend money directly to businesses but works with approved SBA lenders like banks and credit unions to provide loans with favorable terms to small businesses that might otherwise struggle to obtain financing.

Connect with your local SBA branch to talk to experts, mentors, and counselors who can help you learn about the different types of loans you may qualify for and how to improve your application.

They’ll be able to walk you through the various options available to you, such as the different types of loans and grants you may qualify for, as well as help you draft or review your application.

3. Review different small business lenders

There are a variety of small business lenders out there, from traditional bank loans to SBA loans and online lenders. Which one you should approach first depends on what you do and how much you need.

Before choosing a lender, take a look at:

- The types of small business loans that they offer

- What their approval requirements and processes are

- Their interest rates and loan terms

- What they require in return (collateral)

- Whether there are application fees

- Any restrictions (like if you can use it for debt consolidation)

Make sure to compare various lenders to ensure that you get the best loan terms.

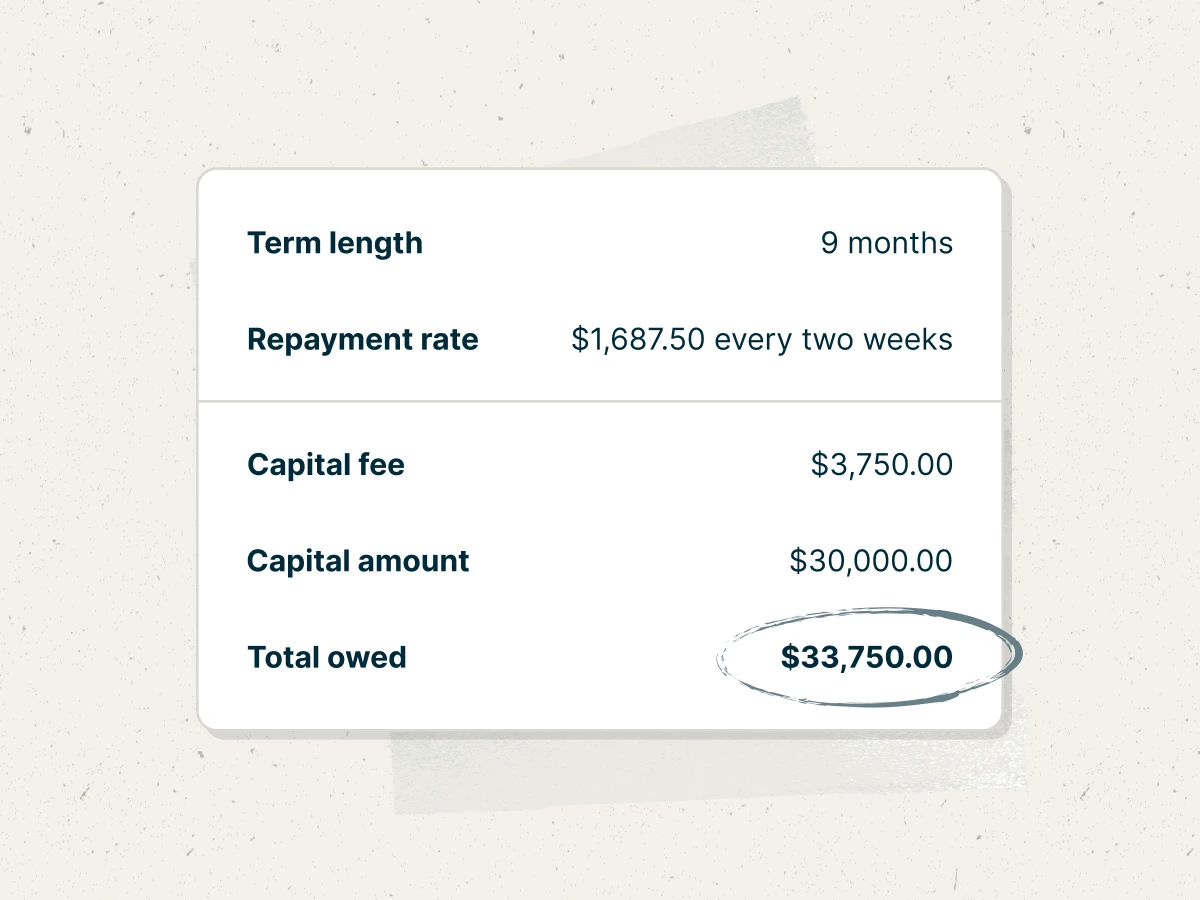

For example, if you want to know what you’ll owe upfront, options like Jobber Capital offer fixed fees and flexible repayment options, giving you more control over your cash flow.

4. Determine your eligibility

Once you know what type of loan you want and how much you need, make sure that you meet the lender’s loan requirements.

Depending on the lender, they may review the following criteria when deciding on your loan application:

- Credit score and full credit report

- How long you’ve been in business, and whether you have a business license

- Collateral or personal guarantee

- Repayment terms

Pro Tip: If you are worried about repayment, you can also explore grants like Jobber Grants, which don’t have to be repaid at all.

Although grants can be more competitive than loans, the application process tends to be more lenient, which makes it easier for small business owners and home service providers to apply for this alternative financing option.

This grant helps me get closer to my goal of making my business my full-time job and be the way that I provide for my family.

5. Create (or update) your business plan

Whether your business is new or has been around for a few years, small business loan lenders will likely ask to see your business plan.

A business plan is a document that outlines the financial and operational aspects of your business, as well as its viability, including industry competitors and risks. It helps lenders understand what your business is and how you plan to grow it in the future.

A typical business plan includes the following information:

- Company details, such as the structure (sole proprietorship, partnership, incorporation, etc.)

- What services you provide and who your target market is

- How much each of your services costs, and whether you offer financing to your customers

- What your advertising and marketing strategy is, including budget

- Who your local competitors are

- A SWOT analysis (strengths, weaknesses, opportunities, threats)

- Operational details, like how your business runs day-to-day and the small business apps you use

- Staff details, like number of workers and whether they’re employees or contractors

- Financial records, like annual expenses, revenue, etc.

The more information you have in your business plan, the easier it is for lenders to understand how you will use a loan to expand and improve your business.

Spend time doing your research for each section so that you’re well-informed and ready to impress lenders.

6. Gather your service business’s financial information

On top of the information you include in your business plan, you may also need more detailed financial material, such as:

- A valuation

- A business credit report

- Year-over-year financial statements and history

- Profit and loss statements

- A business forecast for 1, 3, and 5 years into the future

- Tax returns from previous years

READ MORE: 30 small business tax deductions to save money when filing

Keep in mind that any projections you make should be based on accurate and realistic estimations.

Use numbers from previous years to inform your predictions and make sure that you understand them well enough to explain why you need a loan and how it will help you to grow.

7. Apply for a small business loan

Now that you know how to get a small business loan, all that’s left to do is to apply.

The application process differs depending on the lender you choose. For online lenders, the small business loan process is often entirely online, and the application is often quick and automated.

On the other hand, traditional banks and credit unions often require you to go into a physical branch or over the phone.

Pro Tip: Before submitting your application, have an expert or someone from your local Small Business Development Centre look over it to help avoid delays in processing.

8. Get approved and review your loan agreement

If you get approved for a small business loan, congratulations!

Make sure to review your loan agreement thoroughly and ensure that you understand the repayment terms. If you have any concerns, have a lawyer look over it as well.

You should receive your funds once you sign your loan agreement. Then, it’s time for repayment. Double-check the frequency and amount of your payments (bi-weekly, monthly, etc.) to avoid making late payments.

Timely payments will boost your business and personal credit scores, ensuring that you’ll be able to qualify for a loan again if you need one to scale your business.

Plan B: What if you’re not approved?

There may be circumstances where your loan application is rejected. If this happens, don’t worry, as you have other options:

- Apply with a different lender. For example, if you went with a traditional bank the first time, you may want to try an online lender the second time.

- Consider small business grants: Grants are free money, so they tend to be competitive. However, they are worth applying for. You can obtain grants through the local, state, and federal government, or private entities such as Jobber.

- Crowdfunding: Crowdfunding platforms such as GoFundMe can be an effective funding option, especially if you already have a loyal customer base. It’s important to note that these platforms typically take a percentage of donations for use of their website.

If you were rejected due to a bad credit score, you could also take time to work on your credit and then submit another small business loan application in a few months.

Frequently Asked Questions

-

The credit score needed for a small business loan depends on the type of loan and the lender’s specific requirements.

Generally, traditional banks and the SBA prefer a credit score of 680 or higher, while alternative lenders and online lenders may accept lower scores, sometimes as low as 500-600. -

While it’s best to have a good credit score, don’t let a bad credit score stop you from applying.

Some alternative lenders, online lenders, and certain SBA loan programs may approve borrowers with scores as low as 500-600.

For example, SBA microloans are smaller loans available for small business owners who may not qualify for traditional financing.

However, some alternative loans often have higher interest rates, which means they may require higher payments or take longer to pay back. -

Generally, most lenders require businesses to be at least 6 months to 2 years old before approving a loan.

However, every lender has their own rules. The length of time you need to be in business to qualify for a small business loan depends on the lender and loan type. -

Getting a business loan without collateral can be challenging but not impossible.

Many traditional lenders, such as banks, prefer secured loans backed by collateral such as real estate, equipment, or inventory to reduce their risk. However, you can possibly get an unsecured loan with:

• A good credit score

• Proof of strong business revenue

• Low debt-to-income ratio

• Higher interest rates -

The main difference between a grant and a business loan is that a grant does not need to be repaid, while a loan must be paid back with interest.

Although grants can be competitive, it is always worth applying for them as they allow you to secure funding without debt.

Start by taking 5 minutes to apply to the Jobber Grant program for a chance to gain funding to take your home service business to the next level. -

Yes. Eligible Jobber customers can access financing options through Jobber Capital. Once approved, funds are typically deposited within 1-2 business days. Repayment terms are clear and flexible, helping you maintain control over your cash flow.

You can also extend financing to your customers with consumer financing options. Ideal for bigger jobs, consumer financing can provide your customers with flexibility plus help you get paid up front for your work.